Here is a detailed breakdown of what’s currently on the market to help you decide

You have some cash that you don’t want to see dwindle away thanks to inflation, and you’re looking for the best place to put that money to work. You want appreciation for your capital and you have a particular risk profile that you are comfortable with. A Short-term note looks good, but there are lots to choose from and you’re not sure which would be best for you.

We have created this guide to give you the most detailed breakdown possible. You’ll find the right information so you can make a decision you feel good about. We are assuming you already know what a short-term note is, and you are trying to choose between different types. If you are looking for more personal guidance, contact us.

So, let’s get started by outlining the advantages and disadvantages you might be facing to make sure we are all on the same page before we get into the details of different note types.

Advantages and disadvantages of a short-term note

First, the good stuff:

- Time scale: As the name suggests, a short-term note only ties up your capital for a limited amount of time, usually 2 years or less. This is great if you are looking to park your capital somewhere that will likely perform better than just holding cash, but you also want to have the flexibility of accessing your money for other opportunities within the next two years.

- Low risk: A short-term note is generally considered a low-risk investment since they are typically issued by the government or highly rated corporations and mature in a short period of time. You might also hear them being called ‘short-term debt securities’.

- Liquidity: A short-term note tends to be pretty liquid, which means that it can be easily sold and converted back into cash. Liquidity is useful if you think you might need quick access to your funds for other things in the near future.

- Predictable returns: The interest rate on quite a few short-term investment notes are fixed, like Treasury Bills for example. Treasury Bills are one type of government-issued fixed-income security that might be a good option for you if you are looking for a very low-risk, guaranteed return on investment.

Next, the drawbacks:

- Low returns: Low returns are often the trade-off you will get in exchange for the lower risk profile of a short-term note. This tends to be more true for fixed-income notes. There are a number of short-term note options on the market which are not fixed income, and therefore offer higher potential yield alongside a higher risk profile. We will cover those in this blog.

- Limited accessibility: Short-term investment notes are typically only available to accredited investors or through investment brokerages. You might not be able to access some short-term notes without professional assistance. This is true for the notes we provide, for example, because we specifically serve accredited investors and registered investment advisors.

- Interest rate risk: Interest rates can change rapidly, as we have seen over the last 12 months. These fluctuations can cause the market value of a short-term note to dips, which can result in a loss of value if you need to sell your investment before maturity. For some notes, you can’t sell before maturity – your capital is locked in until the end of the investment term.

Ok. So, you’re familiar with the pros and cons and you think that short-term notes are a good option. The next question is, which products to choose?

Next, we move on to a rundown of the different types of short-term not out there. The list below is comprehensive but not complete – we have focussed on the most popular kinds of short-term notes as these are most likely the ones you are trying to choose between.

Comparison of different types of short-term notes

- Treasury bills (T-bills): Treasury bills are issued by the US government and are considered to be one of the safest short-term investments. They have a maturity period of less than one year and are auctioned off by the government on a regular basis. T-bills offer low returns, but they provide a low-risk option for investors.

- You can buy T-bills directly from the government, or you can get your broker to handle them for you. Over the last 10 years, the average return of a US T-bill has been somewhere around 4%.

- To put that in context, 2022 showed an annual inflation rate of 8% which means that your T-bill would have lost roughly half its value last year.

- Having said that, the overall average inflation rate in the US over the last 10 years has been 3.8%, which means you would have gained a tiny little bit of return if you had held your T-bill for 10 years.

- Commercial paper: Commercial paper is issued by corporations and is used to finance their short-term needs. It has a maturity period of less than one year and is typically issued in pretty huge denominations (think $1,000,000+), which means you probably couldn’t invest in it unless you represent an institutional investor. Commercial paper offers slightly higher returns than T-bills, but it also carries a higher level of risk because they are not government-backed.

- Bank Certificates of Deposit (CDs): CDs are issued by banks and have a fixed interest rate and a set maturity date. They are considered low-risk investments and provide predictable returns. CDs typically have a minimum investment requirement and a penalty for early withdrawal, which you might not mind as long as you definitely don’t need to access the capital for the entire term of the note.

- Merchant Cash Advance Investing: Merchant cash advance investing involves lending money to businesses in exchange for a percentage of their future income.

- It might help you to think of it like buying a pair of shoes in advance. The shoemaker needs cash to make the shoes. You lend her the cash, you get some of the shoes once she has made them. Like that, but with cash rather than shoes.

- MCA investments are really flexible – you can find short, mid, and long-term note products.

- They tend to be considered higher risk than T-bills or CDs due to the possibility of default by the borrower.

- MCA investing is what we specialize in. You can read a full explanation of exactly how they work from start to finish here.

- Real Estate Investing: You can invest in real estate investing as a short-term investment if you buy into a specific project or through commercial short-term real estate notes. You can expect to have your capital tied up anywhere from a few months to several years and returns can vary widely depending on the type of investment and the market conditions. Real estate investing is considered a high-risk investment due to the likelihood of market fluctuations and default by the borrower.

- Collectibles Investing: Collectibles investing involves buying and selling things like rare or old coins, stamps, and art. You can hold them as either short or long-term investments.

- You would most likely be looking to invest through a broker like an art gallery if you are interested in investing in a particular creator.

- There are also ways to invest in fractionalized collectibles. Basically, this means that the coin or stamp or painting is ‘broken down’ (it’s not actually broken down) into, say, 100 pieces and you can buy one or more of these 100 pieces. It is a similar process to buying shares in a company.

- Collectibles are considered high-risk because there is a much more limited market for stamps and coins and art than there is for real estate or loans, for example.

- Collectibles also carry an increased risk due to the possibility of fraud.

Alright, so now that we have explored the most common types of short-term notes we are going to cover the factors that will impact the return on your investment in whichever type of note you decide to invest in.

You already know that any investment is influenced by a combination of things like interest rates, market conditions, and the creditworthiness of the issuer. But these factors are worth saying a little more about.

You are a smart and diligent investor, which is why you are here, learning. We want to make sure that we give as much value as we can here, hence the detail.

Ok, let’s go.

What impacts the yield of short-term notes?

- Interest Rates: The return on short-term investment notes, like Treasury bills, commercial paper, and bank certificates of deposit (CDs), is influenced by the prevailing interest rates in the market. When interest rates rise, the yield on short-term investment notes will also rise. However, you guessed it, when interest rates fall, the yield on your short-term investment notes will also fall.

- Interest rates are especially relevant to fixed income notes because even in undesirable interest rate environments, private companies can remain profitable and can pass on that return to you. This is part of the reason why we think MCAs can be such a great addition to a portfolio since their diversity can hedge against inflation-related losses. More on this later.

- Market Conditions: The demand for short-term investment notes is also influenced by market conditions. During periods of economic uncertainty, like now, you might be more interested in higher-yield products to compensate for the increased riskiness of the market as a while.

- Luckily for you, this overall increased demand for higher yields will push up the yield on short-term investment notes.

- Conversely, during periods of economic stability and growth (not like now), you might be more willing to accept lower yields, which will result in lower yields on short-term investment notes. Pretty logical.

- Creditworthiness of the Issuer: This is a big one. The creditworthiness of the issuer is a key factor that impacts the yield of short-term investment notes. You will very likely want a higher yield on short-term investment notes issued by private companies because there is always the risk that their plans might not come to fruition, they might go bust, etc.

- You will also want much higher yields if you invest in notes from a company with a lower credit rating or a history of financial problems, again, because there is a higher risk of default.

- On the other hand, short-term investment notes issued by companies with a strong credit rating and a solid financial history will typically have a lower yield, because, you guessed it, there is a lower perceived risk of default. This is why T-Bills and other state-backed notes have such low returns.

Tax implications of short-term investment notes

Tax is always an important consideration in your overall financial plan and in how you are going to work strategically toward your goals. The tax implications of short-term investment notes in the United States are governed by both federal and state tax laws and regulations. These implications can have a significant impact on the return on your investment.

We have put together an outline of things to think about below, but we are not tax people, we are investment people, so please speak to your financial adviser or accountant for your more specific questions.

Federal Tax Laws:

- Interest income from short-term investment notes is considered taxable income and must be reported on your federal tax return.

- The current federal tax rate on interest income ranges from 10% to 37% depending on your taxable income and filing status.

State Tax Laws:

- Some states have their own tax laws regarding interest income, and the rate may differ from the federal tax rate. It can get confusing. Speak to your accountant.

- Some states do not tax interest income at all, while others may have a lower or higher tax rate compared to the federal rate.

- Basically, check the tax laws of the state you live in to determine what state tax rate you should be paying.

Tax-Exempt Interest:

- Short-term investment notes issued by certain tax-exempt entities, such as state and local governments, may be exempt from federal and/or state income taxes.

- Again, check the tax status of the issuer before investing in tax-exempt short-term investment notes.

We are onto the home stretch. Now we are going to collate everything you have learned in this blog and take you through a checklist.

Finally, use these criteria to assess the short-term investment notes you are considering:

Go through this list like a checkbox and answer each of the questions. Then compare the specific note product you are considering against it.

- Liquidity: Will you need to access your funds quickly in an emergency? Can you cope financially with not touching your investment capital for 1 year, 2 years, or 3 years? Does the product have any early exit charges?

- Credit Quality: How confident are you that the issuer will repay your principal and your interest? How much risk do you have the appetite for?

- Are you prioritizing high growth and larger yields?

- Can you find an issuer who offers a high yield for a product that has a higher risk profile, but the issuer themselves are decent and have a strong track record?

- Maturity: How long do you want to put your money to work? Do you have an acceptable spread of short, mid, and long-term investments to suit your risk appetite and meet your goals?

- If you are looking for a selection of short-term notes, can you find some that are ultra-short (12 weeks), some that are mid-short (1 year), and some that are on the longer side of short (2 years).

- Remember, the shorter the maturity, the lower the risk of interest rate changes, but the lower the return is likely to be.

- Personal Risk Profile: This is really the most important thing for you to have a good grasp on. Are you a thrill seeker?

- Do you have an entrepreneurial streak that makes you want to dabble in a selection of high-risk, high-reward investments?

- Or do you like to play it slow and steady? How much of your principal can you afford to lose? How much are you aiming to gain?

- Financial Goals: Your financial goals underpin this entire process. If you are looking for income, you might prefer investment notes with higher yields.

- If you are looking for stability, you might go for notes with lower yields but lower risk.

- Are you aiming to grow your capital in order to buy a house in 5 years, or are you just experimenting with different investment options for fun and education?

You have covered a lot in this blog post, well done. We hope that you feel a greater sense of clarity and will find it a bit easier to pick the direction you want to go in with your short-term investments.

If you want to make it easier still, we have a great option for you.

You might like our 12% note

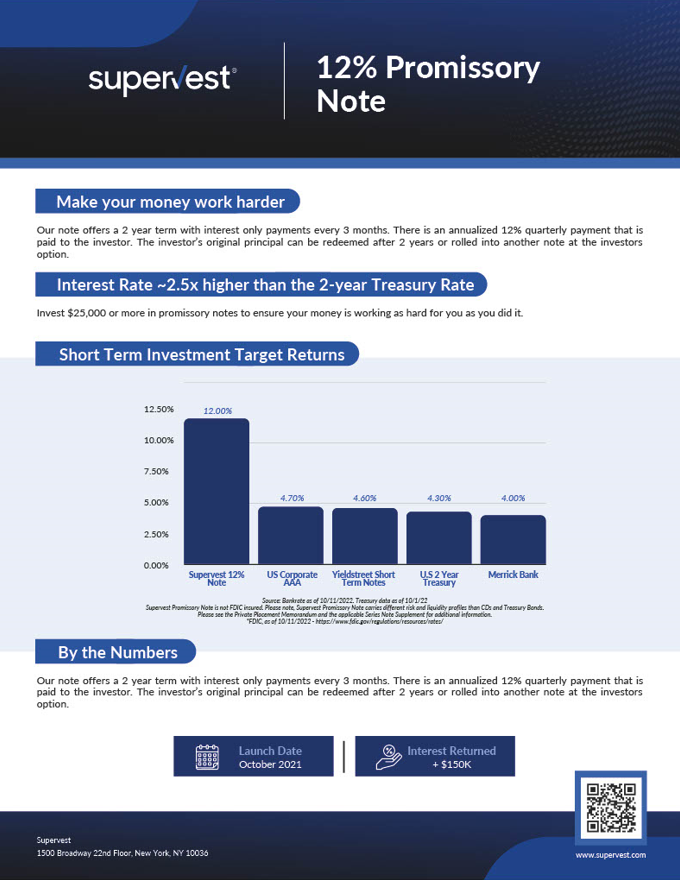

We have a short term note product that we think is great. You might not be looking to invest right now, and if you’re not, that’s fine. But if you are looking to add a high-yield short-term note with tons of built-in diversification, then you might like our 12% 24-month note.

Here are the things you most likely want to know about it:

- It gives you interest-only payments every 3 months for some helpful extra income.

- Your original principal can be redeemed after 2 years or you can roll into another note.

- Your capital is locked into the basket of investments that we oversee for the duration of the 24 months.

- It aims for a 12% yield which is a really strong return for a short term note

- For comparison, our note aims to bring you an interest rate that is 2.5x higher than the 2-year Treasury rate

- We do a LOT of due diligence on our MCA investments to make sure your money is as safe and as hardworking as possible. Some of the things we do include:

- Third-Party Assessments

- OFAC / CLEAR Report (supply chain risk assessment etc)

- In-person site visits

- In-depth compliant review of financials including balance sheet reviews, underwriting analysis, static pool assessments, and collection guidelines

- AML monitoring

- We also use proprietary AI to analyze funder and deal-level performance to bring you the best results through the most profitable deals

If you want to diversify your portfolio and get started with a really strong 12%* 24-month note, you can do that here.

We are looking forward to having you on board.